How Your Enrollment Status Affects Financial Aid

Dropping one class mid-semester sounds like a personal academic decision. For a lot of students, it is. But for students receiving federal financial aid, that single dropped class can slash a Pell Grant, cancel a loan disbursement, and trigger a bill for money already spent on rent. The rules aren't hidden — they're just never explained upfront, and by the time students find out how the system works, they're already on the wrong side of it.

Here's what you actually need to know.

The Four Enrollment Tiers That Drive Everything

Federal financial aid doesn't care whether you feel like a full-time student. It tracks a specific number: your enrollment intensity, defined by the 2025-2026 FSA Handbook as "the percentage of full-time enrollment at which a student is enrolled, rounded to the nearest whole percent."

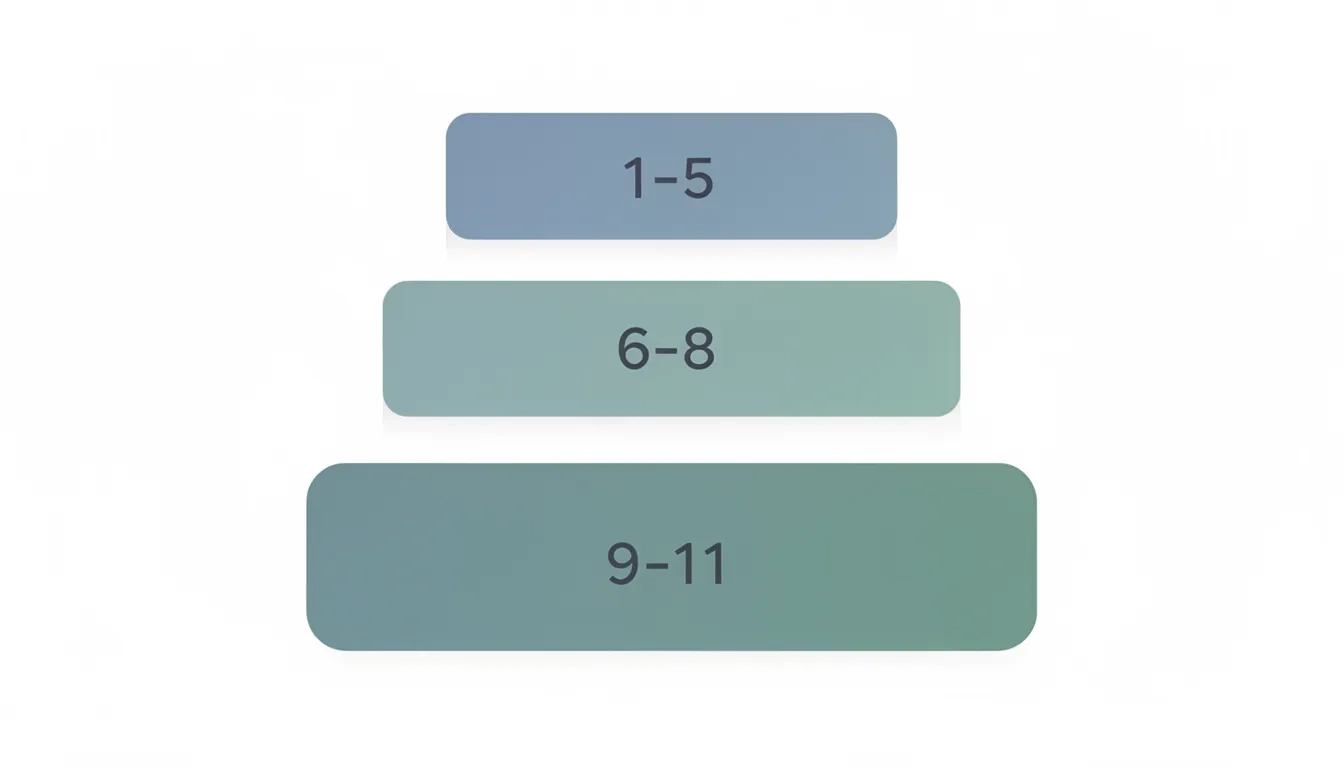

Most colleges define full-time as 12 credit hours per term. From there, the federal government recognizes four distinct enrollment levels:

| Enrollment Status | Credit Hours Per Term | Enrollment Intensity |

|---|---|---|

| Full-Time | 12 or more | 100% |

| Three-Quarter Time | 9–11 | ~75–92% |

| Half-Time | 6–8 | ~50–67% |

| Less-Than-Half-Time | 1–5 | Below 50% |

These thresholds are standardized across federal programs, though individual colleges can set stricter definitions for their own institutional aid. Many do.

One thing worth knowing upfront: enrollment intensity is capped at 100% for Pell Grant calculations. Taking 18 credits won't earn you a bonus. You're already at ceiling.

How the Pell Grant Scales With Your Course Load

The Pell Grant is the most flexible of the federal aid programs when it comes to enrollment. Unlike loans, which have a hard cutoff at half-time, Pell Grants are available at every enrollment level — including less-than-half-time. But the amount shrinks proportionally as your intensity drops.

The 2025-2026 maximum Pell Grant is $7,395 per academic year. That's for a student with a zero Student Aid Index (SAI) attending full-time for a complete academic year. At half-time (50% intensity), that same student would receive roughly $3,697 — exactly half. At three-quarter time, they'd receive around $5,546.

Three-quarter time is the option most students skip over. Nine credits is genuinely manageable for students balancing jobs or family obligations, and it still yields 75% of the Pell award. The step down from 12 to 9 credits feels small academically. The aid math reflects that.

Less-than-half-time is a different story. Not only does your Pell award drop below 50% of the maximum, but your Cost of Attendance gets trimmed. The FSA Handbook specifies that housing, food, and personal expenses are excluded from COA calculations for less-than-half-time students (after they exhaust a three-semester allowance). This reduces the Pell calculation further — beyond what the intensity percentage alone would suggest.

"The Scheduled Award is the maximum amount a student can receive during the award year if the student attends full time for a full academic year." — 2025-2026 FSA Handbook, Vol. 7, Ch. 2

Federal Loans: Six Credits Is the Floor

Here's where the rules stop being graduated and start being binary. Federal Direct Loans — subsidized, unsubsidized, and PLUS — require at least half-time enrollment. Six credit hours is the minimum. Drop to five, and those loans are gone for that term. Not reduced. Gone.

This catches students at three common pressure points:

- Withdrawing from one course that pushes them from 6 to 5 credit hours

- Registering as a part-time student without knowing loans require half-time status

- Having a class cancelled by the school and not replacing it

Schools are required to confirm half-time enrollment before disbursing Direct Loan funds. If a student drops below the threshold after receiving a disbursement, the school must halt any further loan payments for that term.

There is a narrow exception buried in the FSA Handbook: if a student only temporarily drops below half-time within a payment period and then resumes at least half-time enrollment in the same payment period, the school may still process the loan disbursement. "Temporarily" does a lot of work in that sentence — schools document these situations carefully, and students should not count on this provision without talking to their financial aid office first.

The 120-day window is also relevant here. Direct Loan funds returned within 120 days of disbursement are treated as a full or partial cancellation, with adjustments to fees and interest. Past that window, more complicated rules apply.

Other Aid Programs: A Mixed Picture

Not every federal aid program follows the same rules. Understanding which programs require what is worth a few minutes of your time before you register.

Programs and their enrollment requirements:

- Federal Supplemental Educational Opportunity Grant (FSEOG): Generally requires at least half-time enrollment. FSEOG is campus-administered, so specific school policies vary — but half-time is the practical floor.

- Federal Work-Study: Half-time enrollment is typically required. Schools rarely assign work-study positions to students carrying fewer than 6 credits.

- TEACH Grant: Requires full-time enrollment in most circumstances. This is the strictest of the major federal grant programs for enrollment purposes.

- GI Bill (Chapter 33): Operates on its own intensity scale. Full-time students receive 100% of the Monthly Housing Allowance (MHA). Three-quarter time students receive 80%. Half-time students receive 50%. The rate is tied directly to enrollment certification each term.

Then there's institutional aid — the elephant in the room. Scholarships and grants awarded by your college typically require full-time enrollment (12 credits). Many private scholarships carry the same requirement. A student who drops from 12 to 9 credits to accommodate a demanding job may keep 75% of their Pell Grant while losing an entire institutional scholarship. The two systems don't communicate with each other, and the shortfall usually surfaces when the tuition bill arrives.

What Happens When You Drop a Class After the Semester Starts

This is where the most painful surprises happen. Dropping a course mid-term isn't just an academic adjustment — it can trigger a retroactive financial aid recalculation.

Here's the sequence when a student drops from full-time to below half-time after the semester has begun:

- The school identifies the enrollment change

- Pell Grant is recalculated based on actual enrollment for that payment period

- If the student already received a full-time Pell disbursement, they may owe money back

- Any undisbursed loan funds for the term are cancelled

- The school halts further loan disbursements and may need to return previously disbursed funds

The census date — typically the end of the add/drop period — is when schools officially report enrollment to the federal government. Many students assume the last day to drop academically is the same as the last day it matters for financial aid. It isn't. The academic withdraw deadline and the financial aid census date are often weeks apart, and changes after census still affect aid calculations through a separate process.

One frequently missed point: a full withdrawal from all courses triggers the Return of Title IV (R2T4) calculation, which is a different and generally more severe process than dropping a single class. Partial drops trigger enrollment status recalculation. Full withdrawals trigger R2T4. These are not the same thing, and students sometimes discover this distinction at the worst possible moment.

State Aid: Often Stricter Than Federal Rules

Federal aid gets most of the attention in enrollment conversations. State grant programs are frequently stricter — and students who rely on them need to read those requirements separately.

The majority of state grant programs require full-time enrollment for full awards. New York's TAP (Tuition Assistance Program) requires full-time status for freshmen and sophomores (with limited partial awards) and then full-time status for juniors and seniors to receive any funding at all. California's Cal Grant, Texas's TEXAS Grant, and similar programs all set their own enrollment minimums that are independent of federal rules.

The federal floor is not the state floor. A student who drops to 9 credits (three-quarter time) may remain fully eligible for federal Pell and loan aid while losing their state grant entirely. Checking state program requirements specifically — not just assuming they mirror federal standards — is something too few students do before reducing their course load.

Planning Your Credit Load Around Your Aid

The honest reality is that full-time enrollment is financially rewarded by nearly every aid system, but it's not achievable for everyone. Working parents, students managing health conditions, and first-generation students navigating family obligations often can't take 12 credits. The financial aid system was largely designed around a student who does nothing but study — and that describes a shrinking share of actual college students.

Given that, here's a practical decision framework based on where you land:

If you're deciding between 12 and 9 credits: Check whether any institutional scholarships require full-time status before stepping down. Many have appeal processes for medical or financial hardship that can preserve the scholarship at 9 credits if you ask. Federal loans and Pell remain available at 9 credits.

If you're deciding between 6 and 5 credits: Six credits is the floor for federal loans. At five, you keep some Pell Grant but lose loan access entirely. Private loans fill the gap for some students, but they carry higher rates and fewer protections than federal options.

If you're already enrolled and considering dropping a class: Talk to financial aid before you withdraw. Ask specifically about your census date, whether the drop crosses a threshold, and whether it creates any repayment obligation for the current term. This conversation takes 15 minutes and can prevent months of billing headaches.

Students who figure out these rules before registering consistently avoid the worst situations. This isn't about finding loopholes. It's about understanding a system that already knows all the rules — and making sure you do too.

Bottom Line

The six credit hour threshold is the single most important number in federal financial aid. Below it, federal loans disappear. Above it, most federal programs remain available at reduced levels.

Here's what to act on:

- Before registering: Verify whether any scholarships or grants require full-time (12-credit) status and plan accordingly

- Before dropping a class: Ask your financial aid office about your census date and whether the change creates a repayment obligation

- If you're a consistent part-time student: Build your financial plan around Pell and grants rather than loans — loan access at fewer than 6 credits doesn't exist

- If you receive state grants: Read those eligibility requirements separately; they are often stricter than federal rules and governed by a different agency entirely

The system penalizes part-time students in ways that are genuinely out of proportion — particularly working adults and caregivers who have no realistic path to full-time enrollment. That's worth naming. Until the rules change, knowing exactly where the thresholds are is the most useful thing a student can do.

Frequently Asked Questions

Does enrollment status affect financial aid differently in the summer?

Yes. Summer terms are treated as a separate payment period, and Pell Grant eligibility in summer is based on whatever Pell eligibility remains after fall and spring. Federal loans still require half-time (6 credits), but some schools use compressed credit-hour definitions in accelerated summer sessions — 6 credits in a 6-week session might qualify as full-time for housing allowance purposes. Check with your financial aid office specifically for summer, as summer rules can diverge from the regular year.

Can I get any financial aid as a less-than-half-time student?

The Pell Grant is available below half-time, but with meaningful restrictions. Your Cost of Attendance for Pell calculations excludes room, board, and personal expenses, which reduces the award beyond what the enrollment intensity percentage alone would suggest. Federal loans are completely unavailable. FSEOG and Work-Study are generally not available. Most institutional and state grants are also off the table. Pell is essentially the only federal option remaining below six credit hours.

Myth vs. reality: Does dropping a class always mean owing money back?

Not always — this is a common misconception. If you drop a course but stay at or above your existing enrollment threshold (going from 15 credits to 12, for example), your aid status doesn't change at all. Repayment risk appears specifically when a drop crosses one of the four enrollment tiers, and it's most severe when dropping below half-time. Changes before the census date have less impact than changes after it. Always check before assuming you owe something.

What's the difference between dropping a class and withdrawing completely, for financial aid purposes?

A full withdrawal from all courses triggers the Return of Title IV funds (R2T4) calculation, which determines what percentage of aid must be returned based on how far into the term you attended. Dropping one class is different — it triggers an enrollment status recalculation, which adjusts aid to match your new credit load. R2T4 is generally the more severe of the two processes. Many students don't know these are separate procedures until they're caught in one of them.

Will taking fewer credits affect my Satisfactory Academic Progress standing?

Yes, indirectly. SAP requirements track both GPA and completion rate — the share of attempted credits you successfully complete. Dropping courses increases your attempted-but-not-completed credits, which lowers your completion rate over time. Most schools require at least a 67% completion rate to maintain federal aid eligibility. Frequent drops won't immediately trigger SAP failure, but they move the needle in the wrong direction, and students on the margin can lose aid eligibility over multiple terms of reduced completion.

My scholarship says "full-time enrollment required" — is there actually any flexibility?

More than most students assume. Many institutional scholarships have formal appeal processes for documented medical, family hardship, or financial emergencies. Financial aid offices often grant single-term exceptions for students who have been consistently full-time and hit an unexpected obstacle. The appeal rarely gets made because students assume the answer is no and never ask. Ask anyway. A 15-minute conversation with a financial aid counselor has saved more than a few students from losing scholarship funding they were otherwise entitled to keep.