How Federal Aid Programs Interact With Private Aid (And Why It Matters)

Winning a $5,000 community scholarship should feel like a victory. For plenty of students at colleges with strict aid policies, it functionally becomes a $5,000 gift to the financial aid office — not to them. Their college sees the outside award, quietly adjusts the institutional grant downward by roughly the same amount, and the net bill barely moves. That's not a glitch or a clerical error. It's the predictable result of how federal rules and institutional policies stack together — and understanding those mechanics is worth real money.

The One Rule That Governs Everything

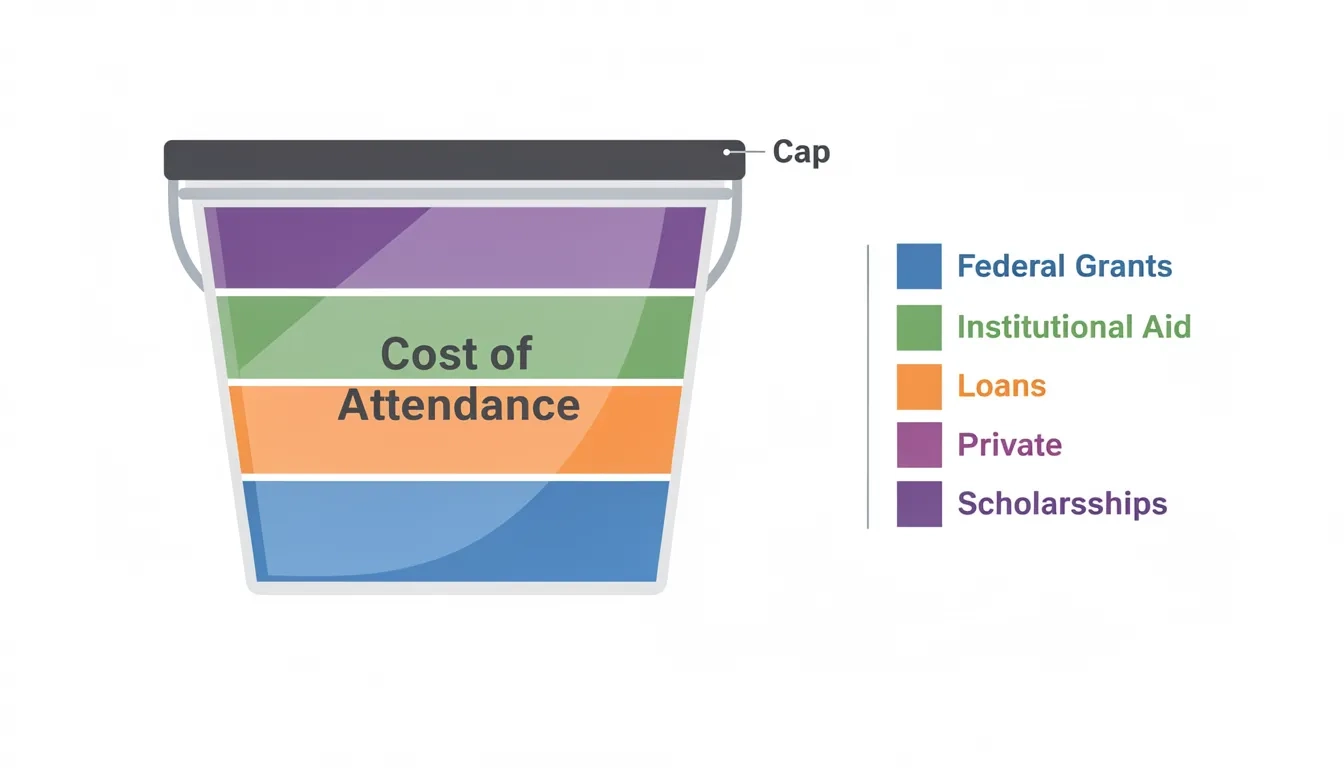

Total aid cannot exceed your cost of attendance. That's the master constraint that every other rule flows from. Cost of attendance (COA) is a school-defined number covering tuition, housing, food, books, transportation, and personal expenses. It's set by each institution annually, and federal law treats it as the ceiling for all aid combined.

Schools build your package using a formula from the 2025-2026 Federal Student Aid Handbook:

COA − Student Aid Index (SAI) − Other Financial Assistance (OFA) = Remaining Need

"Other Financial Assistance" is the bucket that catches everything outside of federal Title IV programs. State grants go in. Institutional scholarships go in. Private outside scholarships go in too.

Every dollar of OFA shrinks the "remaining need" figure. That figure is what need-based federal programs like the Federal Supplemental Educational Opportunity Grant (FSEOG) are designed to fill. So when you report a private scholarship to your school, it doesn't just sit alongside your existing aid — it mathematically compresses what other need-based programs will cover.

Here's what that looks like with real numbers:

- COA: $35,000

- SAI (your expected contribution): $8,000

- Remaining need before outside aid: $27,000

- You report a private scholarship of $5,000 (counted as OFA)

- Remaining need drops to $22,000 — and campus-based aid adjusts accordingly

No wrongdoing. No oversight. Just arithmetic built into federal policy.

Where Pell Grants Stand Apart

Pell Grants are the clearest exception to the outside-aid squeeze. The FSA Handbook says it directly: "a correctly determined Pell Grant is never adjusted to take into account other forms of aid." If you qualify for the maximum Pell ($7,395 for the 2025-26 award year), that amount is locked in regardless of how many private scholarships you've earned. No displacement. No reduction.

This is a deliberate policy choice. Pell functions more like an entitlement for low-income students — a federal commitment made based on family finances, not based on what else arrives in the aid package. Other sources can't override it.

There is one new wrinkle worth knowing. Starting in the 2026-27 award year, students whose combined nonfederal aid — state grants, institutional grants, and private scholarships together — equals or exceeds their full cost of attendance will lose Pell eligibility. For most students that scenario is theoretical. But for students at low-cost community colleges who have secured heavy institutional funding, it's a real risk worth modeling before accepting packages.

The takeaway: Pell is your safest dollar. Protect it by understanding what triggers that new COA-saturation rule.

Scholarship Displacement: The Silent Problem

This is where students get genuinely surprised. Mark Kantrowitz, one of the most widely cited experts on student financial aid, has documented that roughly half of scholarship recipients experience some form of scholarship displacement — where winning an outside award causes the college to reduce its own institutional grants.

About one-fifth of colleges reduce their own grants before they even touch loans when an outside scholarship arrives. That's the harshest version. The student did everything right — applied, competed, won — and still ends up no better off because the school simply redirected its dollars to another student on the waitlist.

Why do schools do this? Colleges distributed $85.1 billion in institutional grant aid in 2024-25, according to College Board data. Those funds are finite, and schools make allocation decisions across their entire enrolled population. When an outside scholarship fills need that the school was covering, redirecting those institutional dollars elsewhere serves more students in aggregate. Defensible from a systems view. Maddening from yours.

The math is cold. You spend 40 hours on scholarship applications, win $3,000, report it faithfully to your financial aid office, and receive a revised package with your institutional grant trimmed by $2,847. Net reduction in your actual bill: $153.

The 5 Displacement Policies Colleges Use

Not every school handles outside scholarships the same way. Policies generally fall into five tiers — and the difference between them is substantial:

| Policy Type | What It Means | Net Impact for Student |

|---|---|---|

| Dollar-for-dollar reduction | Every $1 outside aid = $1 less institutional grant | Zero net savings |

| Fill unmet need first | Outside aid covers your need gap before touching grants | Moderate benefit |

| Replace self-help first | Loans and work-study reduce before grants are touched | Strong benefit |

| Pay other expenses first | Aid covers laptop, insurance, etc. before affecting grants | Strong benefit |

| Replace SAI (most generous) | Grants unchanged until total aid exceeds full COA | Full benefit |

The most generous policy — reducing your family's expected contribution before touching institutional grants — is what schools like Princeton and MIT offer when they commit to meeting 100% of demonstrated need. At those schools, a private scholarship can directly reduce your out-of-pocket cost.

The harshest policy is dollar-for-dollar reduction. If you have no unmet need and no loans in your package, a private scholarship at such a school saves you nothing at all.

Ask about displacement policy before choosing a school. This question belongs in the same conversation as graduation rates and net price — not as an afterthought after you've already committed.

Overaward Rules: When Federal Law Steps In

Displacement is mostly an institutional choice. Overaward resolution is a federal requirement.

An overaward happens when a student's total aid package exceeds their COA. Schools are legally required to fix it before disbursement. The FSA Handbook specifies a clear resolution order:

- Reassess COA first. If the student has legitimate new expenses — a required laptop, unexpected medical costs, a new commuting situation — the school can raise the COA figure. Sometimes this alone eliminates the overaward without touching any aid.

- Reduce unsubsidized loans next. These go first because they're not need-based. Cutting them doesn't strip the student of something they "earned" through demonstrated need.

- Reduce other Title IV aid — subsidized loans, FSEOG, work-study — only after loans are exhausted.

Pell Grants are the last thing touched under this hierarchy. Federal rules protect them even in overaward situations.

There's also a small built-in grace period for campus-based programs: a $300 overaward tolerance. If the overaward is below $300 and the school genuinely didn't know the student would receive outside aid, no corrective action is required. Cross that threshold, though, and the school must act before disbursement — otherwise the overaward becomes an overpayment, which means the student owes money back.

This is why some schools don't flag small local scholarships immediately. Once you're under $300 over, the administrative hassle exceeds the federal obligation.

Strategies That Actually Reduce Your Bill

Understanding how these rules interact makes them workable. Here's a practical sequence:

- Calculate your need gap first. Subtract your full aid package from your COA. If there's still a gap — unmet need — outside scholarships fill that gap without touching any grants. That's where outside scholarships are most valuable.

- Ask your school's displacement policy directly. Call the financial aid office and ask: "If I receive an outside scholarship, do you reduce my institutional grants dollar-for-dollar?" Schools are required to answer this question honestly, and most will.

- Know whether your aid is need-based or merit-based. Merit-based institutional awards typically hold until total aid exceeds COA. Need-based awards are vulnerable the moment your demonstrated need is fully covered. The type of aid you hold determines how risky outside scholarships are.

- Time disbursements to your need profile. Some families report outside scholarships in the year when they carry the most unmet need — often freshman year, before all merit aid layers in. Ask your aid office if scholarship timing affects how displacement is applied.

- Appeal the displacement. Schools have discretion. If a $4,000 scholarship triggers a $3,800 institutional grant reduction, request a meeting with your aid officer and ask whether the package can be restructured. This works more often than students expect.

The system has more flex in it than the fine print suggests.

The Bigger Picture: $173.7 Billion in Moving Parts

College Board's 2024-25 data puts total undergraduate and graduate grant aid at $173.7 billion — $53.7 billion from federal programs, $85.1 billion from institutions, with state and private sources making up the rest. Private scholarships are the smallest slice of that pool, but they're the one students can actively pursue and control.

The interaction between these funding streams is getting more scrutiny. Maryland passed legislation banning scholarship displacement at public colleges, requiring schools to use outside scholarships to reduce student loans and family contributions rather than institutional grants. Other states have started exploring similar rules. The political pressure is real, and the policy landscape is shifting.

My position on this: the current system disproportionately punishes motivated students from middle-income families. Low-income students with large need gaps benefit from outside scholarships without displacement risk. High-income students rarely rely on institutional grants in the first place. It's the middle — students with partial need-based packages and no loan cushion — who win scholarships and gain nothing. That's the group most worth advocating for as state legislatures revisit these rules.

Understanding the system as it exists today is still your best defense. Every dollar you save by knowing which school has a generous outside scholarship policy, or by negotiating a displacement appeal, is a dollar that stays in your pocket.

Bottom Line

- Pell Grants are protected from outside scholarship displacement — they're the one federal program that cannot be reduced by private aid.

- Institutional grants are not protected by federal law, and many colleges will reduce them dollar-for-dollar when outside scholarships arrive.

- Ask about displacement policy before choosing a school — it belongs in your comparison process alongside net price and graduation rates.

- If you have unmet need, outside scholarships are genuinely valuable. The problem only bites when your need is already fully covered by existing grants.

- Appeal displacement decisions. Schools have discretion, and financial aid officers often have room to work with engaged families who ask.

The rules are stacked in ways that aren't obvious. But they're knowable — and knowing them is most of the battle.

Frequently Asked Questions

Does winning a private scholarship reduce my Pell Grant?

No. Pell Grants are explicitly protected under federal law — the FSA Handbook states that "a correctly determined Pell Grant is never adjusted to take into account other forms of aid." No matter how many private scholarships you win, your Pell award remains fixed as long as you meet eligibility requirements. The one exception coming in 2026-27 is for students whose total nonfederal aid equals or exceeds their full cost of attendance — an edge case for most students, but worth checking if you're heavily funded.

How do I find out if my college will reduce its institutional grants when I win an outside scholarship?

Call the financial aid office and ask directly for their "outside scholarship policy." Many schools post it on their financial aid website as well. You want to know specifically whether they apply displacement to institutional grants or only to loans and work-study. Some schools have formal written policies; others handle it case by case, which gives you more room to negotiate.

Is it worth applying for private scholarships if my school displaces them?

It depends on your package. If you have unmet need (a gap between your aid package and your COA), outside scholarships fill that gap before any displacement kicks in — making them genuinely valuable. If your need is already fully covered and your package contains no loans, displacement may render small scholarships worthless at schools with strict policies. Larger scholarships that exceed your institutional grant entirely will still reduce your bill regardless of displacement policies.

What's the difference between how need-based and merit-based aid gets displaced?

Merit-based institutional aid is typically only displaced once your total aid exceeds COA — it has a higher tolerance because it was never calculated against your financial need. Need-based institutional aid is far more vulnerable: the moment your demonstrated need is fully covered by a combination of grants and outside scholarships, the school has grounds to reduce its own need-based award. Students with mixed packages (some merit, some need) should check which component their school displaces first.

What happens if my total aid accidentally exceeds my cost of attendance?

This is called an overaward, and schools are legally required to resolve it before disbursing funds. The resolution order under federal rules is: first reassess COA for any legitimate new expenses; then reduce unsubsidized loans; then reduce other need-based Title IV aid. Pell Grants are the last thing reduced. If the overaward is under $300 and the school didn't know in advance, they can let it stand — but above that threshold, they must act.

Do all federal aid programs treat outside scholarships the same way?

No. Pell Grants are uniquely protected and never reduced due to outside aid. Campus-based programs like FSEOG and Federal Work-Study follow the standard OFA formula — outside scholarships reduce remaining need, which reduces these awards. Unsubsidized Direct Loans are not need-based and can cover up to COA regardless of outside aid, so they're typically the last to be affected by displacement and the first to be cut in an overaward situation.

Sources

- Packaging Aid | 2025-2026 Federal Student Aid Handbook

- Overawards and Overpayments | 2025-2026 Federal Student Aid Handbook

- Scholarship Displacement: How Outside Scholarships Affect Financial Aid

- Navigating the 2024-2025 FAFSA Changes: Webinar with Mark Kantrowitz and David Levy

- Packaging & Aid Notification: 2025-26 | NASFAA

- Maryland Bans Scholarship Displacement in Higher Ed